What is an RESP and Why Should I have One?

Jan 15, 2024

As the parent of two teenagers, I think I have a good idea of what it costs to raise them. Over time, costs transition from diapers and new clothes as they continuously outgrow them, to paying for activities and increased food consumption in their teenage years.

One often overlooked cost (or investment, as we see it) is saving for your child’s post-secondary education. The benefits of a post-secondary education (trades, college, university) have been studied for decades, with the overall results indicating a net positive benefit.

And to be honest, it’s fair this cost is sometimes overlooked given other financial pressures of raising a young family. What do you focus on when you have to survive, pay a mortgage or rent, save for an emergency, or for your own retirement.

The Registered Education Savings Plan (RESP) is a savings vehicle in Canada that assists parents wishing to help their children pay for higher education.

How does it work?

An RESP is made up of three different components – your contributions, government grants and growth of the investments.

Contributions

As a parent or grandparent (the “Subscriber”), you can contribute up to $50,000 per child towards their education.

Grandparents, this is a wonderful way to help provide your grandchildren with funds for their future.

Government grants

The federal government adds the Canadian Education Savings Grant (CESG) which matches your contributions at a rate of 20%, up to a maximum of $500 per year (a $2,500 annual contribution from you), to a lifetime maximum of $7,200.

Provincial grants are also available. For instance, BC provides a one-time BC Training and Education Savings Grant (BCTESG) of $1,200 when the child turns 6.

Low income families may qualify for the Canada Learning Bond (CLB), which can provide up to an additional $2,000 lifetime grant.

Growth

Growth on investments (high interest, GIC, bonds, mutual funds, stocks) is tax-deferred until withdrawals are made in the future.

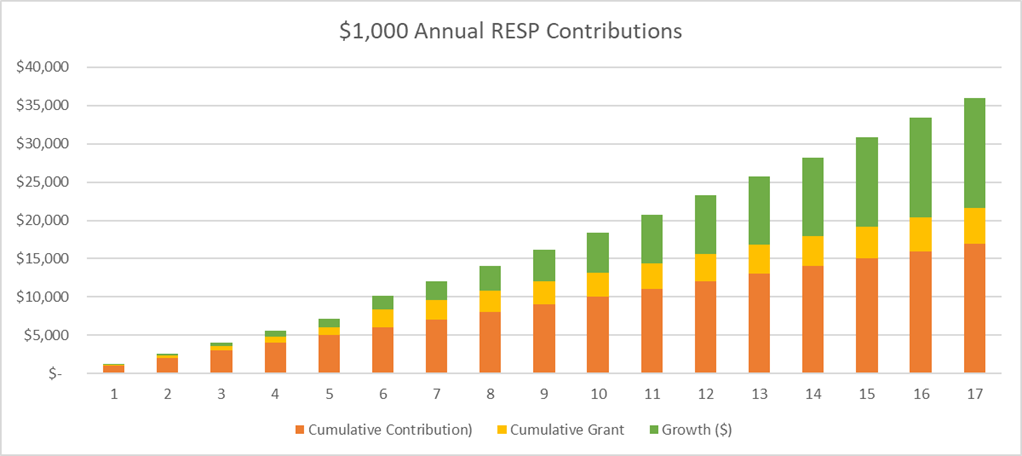

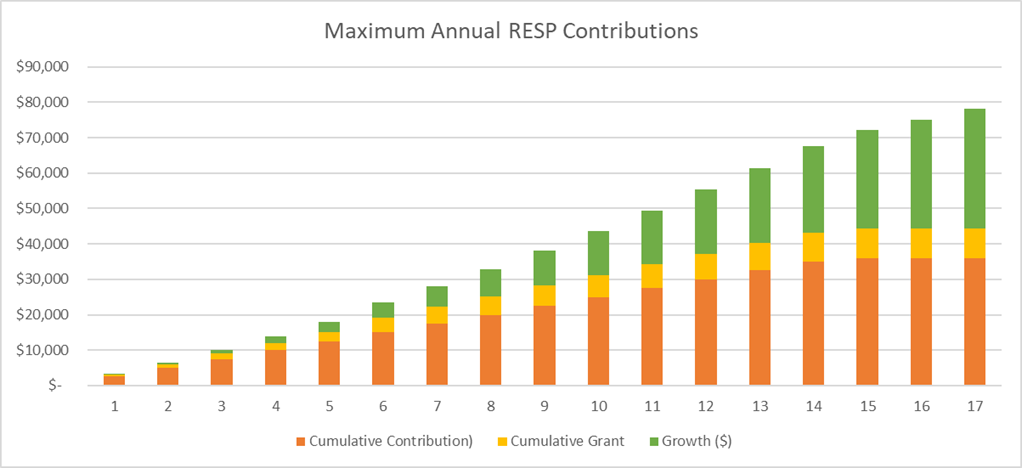

Below are two scenarios illustrating how the RESP could grow over time.

- A family who is able to save the maximum each year to qualify for full CESG, with contributions stopping when grants are maximized

- A family who is able to save $1,000 per year through the child’s age 17

Rate of return – 6% (years 1-12), 5% (years 13-15), 4% (years 16-17)

You can see the benefits of government grants and growth over the 17-year period, greatly increase the amount available to assist students when the time comes – even if you don’t have enough to maximize the entire lifetime contribution amount.

In scenario 1, your lifetime contribution of $36,000 grows to $78,125.67 after 17 years. In the more modest savings scenario, your money still more than doubles from $17,000 to $35,969.40.

The grants and growth do much of the heavy lifting to provide your child with a pot to use towards their continuing education. It also relieves a lot of stress trying to find the money to support them when the time comes.

Now you’re probably thinking, what happens when my child is ready to go to school and is there tax to pay on withdrawals.

Requesting withdrawals

Withdrawals can be made through your RESP provider by completing their required forms and supplying them with a record of your child’s enrollment (i.e., class schedule, registrar letter). They send you a cheque or funds directly to your bank account.

Withdrawals can be made for a variety of different education costs including, but not limited to, tuition, books, and residence costs.

You can request funds from either your contributions (Post-Secondary Education – PSE) or from the growth and grants (Education Assistance Payment – EAP).

PSE withdrawals are not taxable.

EAP are treated as taxable income in the hands of the student (the beneficiary). The advantage is your child is most likely in a low tax bracket, resulting in little or no tax payable.

Qualifying full time course loads allow for a maximum $8,000 EAP withdrawal in the first 13 weeks of the program. There is no limit to the amount of EAP that can be withdrawn after 13 weeks have passed.

Withdrawal planning in the early years of decumulation is important to ensure the growth and grants are drawn out as much as possible first. This allows those portions to be taxed when the child is in a lower tax bracket. It also reduces potential tax in the subscriber’s hands should your child not use all the funds in the RESP.

Qualifying schools

The list of qualifying schools is quite extensive and includes international institutions. A variety of different educational pathways also qualify, including trades, community colleges and full university degree programs.

There is great information available on the Government of Canada’s RESP information page (link below) and your advisor can assist with additional information on structuring investments and withdrawals when your child is ready.

Estate Planning Misconceptions

In this 5-minute webinar, we explore an important but often misunderstood area of financial planning.

Learn More