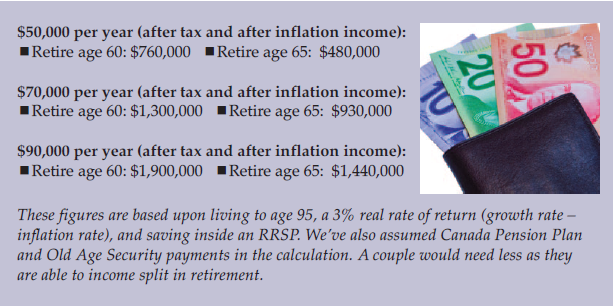

How Much Do I Need to Save to Generate an Income in Retirement?

Jan 27, 2025

This is a complicated question with many variables. We will argue that what you really want to know is what your after-tax income will be over your expected lifetime.

Stages of Retirement Spending

There are three stages to retirement – the first stage is called the “Go-Go” stage, the second the “Slow-Go” stage, and the third is the “No-Go” stage. We would all like to spend most of our retirement in the Go-Go stage of retirement. This stage is typically very active, as your energy is high and you are fulfilling your retirement dreams. The Slow-Go stage is when your energy starts to wane. Your health might not be a major factor, but you just don’t have as much energy as you did earlier in retirement. You probably have seen older relatives or friends go through this stage. The No-Go phase is when your activities are restricted because of health and other physical or mental impediments.

How Much Income Do I Need to Maintain My Lifestyle in Retirement?

A lot of work has been done on this topic. Your so-called “(income) replacement ratio” represents how much of your pre-retirement income you need to maintain your lifestyle in retirement. There is some research that suggests that you only need 50% of your pre-retirement income in retirement, while other studies suggest you need 110% of your pre-retirement income to maintain your lifestyle. The majority of the studies suggest that you need between 60% and 80% of your pre-retirement income to maintain your lifestyle during retirement.

In fact, the right amount is based on what you plan on doing in retirement. Many studies suggest the lower your pre-retirement income, the higher your replacement ratio must be, and the higher your pre-retirement income, the lower your retirement ratio must be. This makes sense because if your pre-retirement income is lower, you’ll use more of it for non-discretionary expenses like rent, food, and other essential spending.

Our Experience

Over the years of helping clients move through retirement, we have seen a different experience.

The first two to three years of retirement tend to be the most expensive, as you are dealing with pent-up demands that you did not fulfil while working full time because you were too busy to do so.

The first two years are often treated like a vacation and can be very expensive.

In some cases, the last two years of retirement can also be very expensive because of long-term care costs.

We’ve also found that our clients do not need to increase their income every year by the rate of inflation to maintain their lifestyle in retirement. In most cases, we find that they usually only need to increase their income every three or four years.

Many of our clients start to slow down later in retirement and spend less money as they become less active. This slowdown in activity tends to become quite pronounced around the age of 80.

If the above spending patterns are true, then you should be able to start with the 1) higher initial withdrawal level; 2) retire earlier; or 3) save less.

We have found that clients can start with an initial withdrawal rate up to 5.5% and maintain their lifestyle throughout retirement.

What Does the Research Suggest?

The major issue we have with much of the research being done about income in retirement is that it assumes retirees need a constant net spendable income (after-tax and inflation) throughout their retirement years.

In 2005, an article by Ty Bernicke “Reality Retirement Planning: A New Paradigm for an Old Science” suggested that under traditional retirement planning, consumers tend to over-save for retirement, underspend in their early years of retirement, or postpone retirement. His research suggested that household expenditures decline as retirees age.

In 2013, David Blanchett wrote a paper called “Estimating the True Cost Of Retirement”. In this paper, he found that retiree expenditures do not, on average, increase each year by inflation. He goes on to suggest that there appears to be a “retirement spending smile” as expenditures decrease in real terms for retirees throughout retirement and then increase toward the end of their lives to deal with health-care costs (US study).

It is important to analyze and design the proper retirement income strategy. ■

Tax Planning

Tax planning can be also complex and hard to understand, because everyone's situation is unique. Below, we look at different financial situations and how we'd suggest each person proceed to get the most favorable result.

Learn More