Hold on Dorothy, We’re Way Beyond Kansas Now!

Mar 19, 2024

In the Land of Oz and the ever-evolving landscape of the stock market, a phenomenon that should capture the attention of investors is a tornado-like concentration of market value within a select few companies. In recent years, the S&P 500 has seen a notable trend in what some analysts have dubbed the "Magnificent Seven" – a group of mega-cap companies whose price changes wield significant influence over the index and, by extension, the broader world markets. Despite this concerning pocket of concentration risk, there is generational opportunity in overlooked small- and mid-size companies that offer distinct value propositions.

The Magnificent Seven (or collectively FAATMAN) – consisting of tech titans like Facebook (Meta), Apple, Amazon, Tesla, Microsoft, Alphabet (Google), and Nvidia – have amassed staggering market capitalizations, (averaging almost $2 trillion each), which exert considerable sway over the index. Their combined weight at almost 30% of the index leads to concerns about top-heavy market concentration risk, as fluctuations in these behemoths can disproportionately impact overall market performance. While the FAATMAN technology sector has fed off the Artificial Intelligence (AI) buffet of speculative disruption, their performance dominance has undermined the importance of diversification.

Unfortunately, this single sector concentration risk may be leading a whole new generation of COVID-converted DIY investors to unwittingly ignore overindulgence in FAATMAN stocks or the indexes they over-weight.

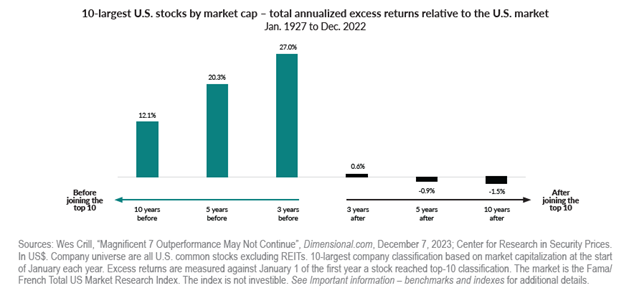

We’ve been through a few of these cycles, coaching investors to stay true to seemingly outdated (at the time) investment principles like: diversify, the law of large numbers, mean reversion, and fundamental value over glamour. I haven’t heard “New Paradigm” on the yellow brick road in a while, but I often hear this time is different. Our experience and advice holds that history may not repeat, but it sure rhymes. Twenty-four years ago, the concentration of the top ten companies reached 20% of the S&P 500 before the Tech bubble imploded. Twenty-seven years before that the “nifty-fifty” era ended with a dismal decade for yesterday’s darling large companies.

This is where small- and mid-size companies enter the spotlight. Although they may lack the market size, and thus representation in the popular indexes, the lack of visibility and analyst coverage to their larger counterparts leads to compelling investment opportunities that are often overlooked. Small-cap stocks, for instance, have historically demonstrated higher growth potential and greater agility in adapting to changing market conditions. Their ability to innovate, expand, and capture niche markets can result in outsized returns for investors willing to embrace proprietary insights on their business models.

Similarly, mid-cap companies occupy a sweet spot between the stability of large-caps and the growth potential of small-caps. They often possess established market positions, solid financials, and room for expansion, making them attractive prospects for investors seeking a more diverse portfolio. Moreover, mid-caps tend to be less affected by geo-political and macroeconomic market gyrations than their larger counterparts, offering a degree of resilience during periods of volatility.

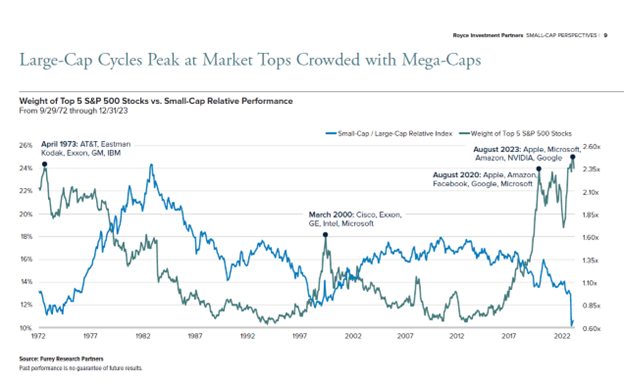

Note in the graph below that, while the largest companies have enjoyed a decade of out-performance distorted by government interventionist policy (monetary, fiscal and COVID), smaller companies are once again poised for a lengthy reversionary period of out-performance. The relative value of small- and mid-size companies is at a generational low making them a compelling inclusion in a well-diversified portfolio.

While the FAATMAN group may command the attention befitting their size, dominant market positions, meta-data sets and AI advantages, their premium valuations, at roughly 30x earnings (the index is 19x on average), mean that smaller companies may present more compelling valuations relative to their earnings potential. Even the next smaller $14 trillion group of 42 large companies in the index have over 2.5x the earnings and 2x the return on invested capital (ROIC) of the FAATMAN group! Additionally, high quality small- and mid-caps can provide exposure to sectors and industries that are underrepresented in mega-cap indexes, offering diversification benefits and potential non-correlated return generation.

In conclusion, while money flowing into the technology sector in the last year has dwarfed all other sector flows combined, the search for the Wizard of Oz has left FAATMAN bloated relative to every other part of the market. Index investors should not overlook the abundant diversified opportunities presented by small- and mid-size companies. The active portfolio managers we work with are diversifying across industry sectors and company sizes researching a broader global universe of investment opportunities while mitigating concentration risk. Ultimately, they will select a portfolio of businesses that represent their focused proprietary insights, based on fundamental business metrics other than total market value.

Why do we plan?

Knowing where you are translates into knowing where you're going, and we hope to provide every client with the trust and confidence to navigate through the waters of their financial lives.

Learn More