Q3 Market Commentary: Key Considerations for Investors as We Approach Year-End

Oct 29, 2024

At the beginning of the final quarter of 2024, several pivotal topics are shaping investor sentiment. Below is a concise summary of five critical themes that are top of mind as we look toward year end and beyond.

1. US Election Landscape

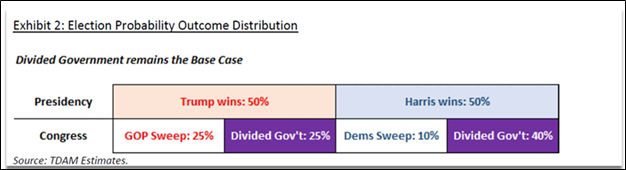

The upcoming presidential election is poised to be a closely contested race, with analysts giving nearly equal odds to Trump and Harris for the Oval Office.

A divided Congress is currently seen as the base case, which historically has been favourable for market performance, particularly in the year following an election.

While concerns about potential tax increases under a Democratic sweep linger, the reality is that significant political changes often face hurdles in a divided Congress. This setup tends to mitigate fiscal and political uncertainty, allowing markets to focus on underlying economic conditions rather than campaign promises.

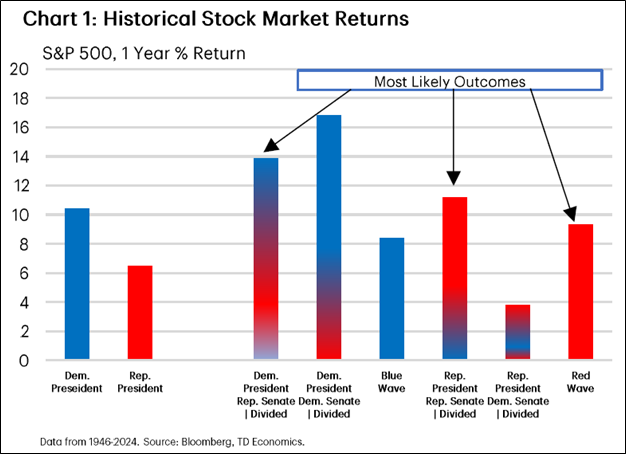

Historically, the state of the economy at the time of a party’s ascension has been more impactful on market performance than the election results themselves.

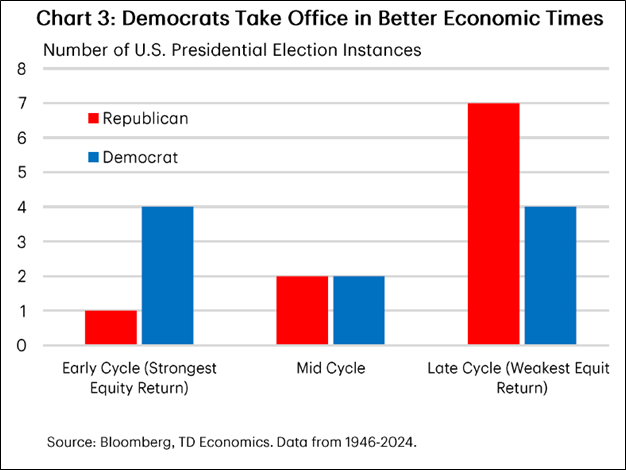

Historically, Democrats have had the fortune of taking office more often in the early stages of economic cycles, when there is the highest potential for the strongest equity return.

2. Economic Outlook

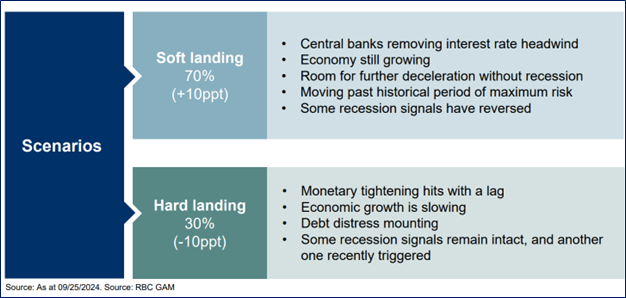

As recession fears dissipate, the outlook for a “soft landing” — characterized by sustained economic growth — has gained traction. This shift provides a more optimistic backdrop for both consumers and investors, reinforcing the notion that the economy may continue to expand rather than contract.

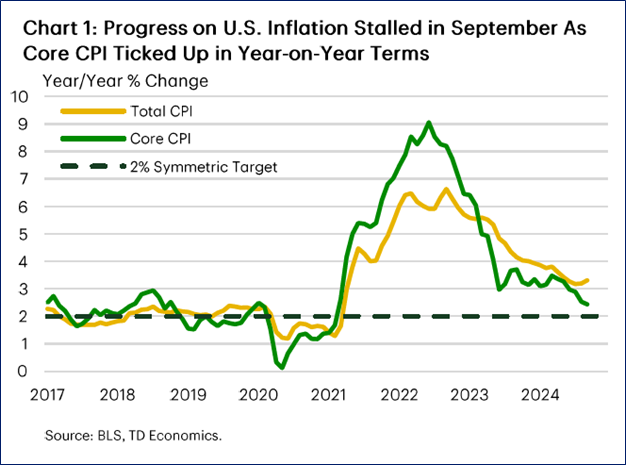

3. Inflation Trends

Inflation has shown signs of cooling, aligning more closely with the targets set by both the Bank of Canada and the US Federal Reserve.

This trend supports the expectation of larger and sooner rate cuts, which could further invigorate economic activity. As inflation moderates, consumer purchasing power may improve, which bodes well for overall market confidence.

The US consumption economy is still considered to be “smouldering” and more resilient than the Canadian economy where consumers are carrying the highest debt loads of the prosperous G10 countries.

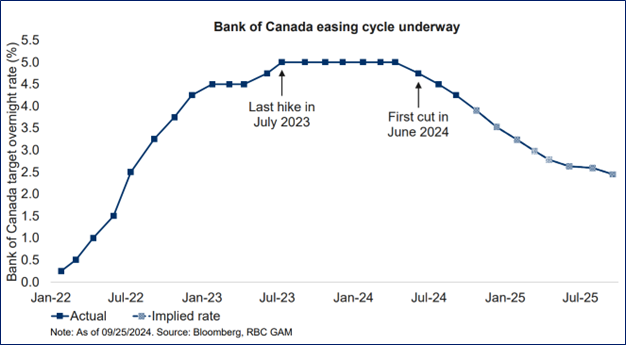

4. Interest Rates and Currency Stability

Canada’s resource-centric export-driven economy without the consumer capacity to spend our way out of a slowdown, has led the Bank of Canada to a more accelerated path of interest rate reductions so far.

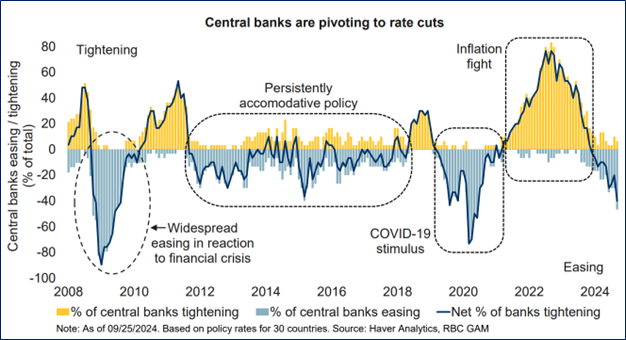

However, Canada is not alone as governments around the world are pivoting from tight monetary policy to lower the very same interest rates they raised in 2022. “Round, round, we go.”

Many countries are anticipated to continue the recent trend of rate cuts, responding to the improving inflation outlook.

Source: RBC GAM, Bloomberg. Rate definitions: U.S.= Fed Funds rate; Canada= Overnight rate; Europe = Eurozone policy rate; United Kingdom= Base rate; Japan= Overnight call rate. * Please note that the forecasts are updated quarterly in March, June, September and December.

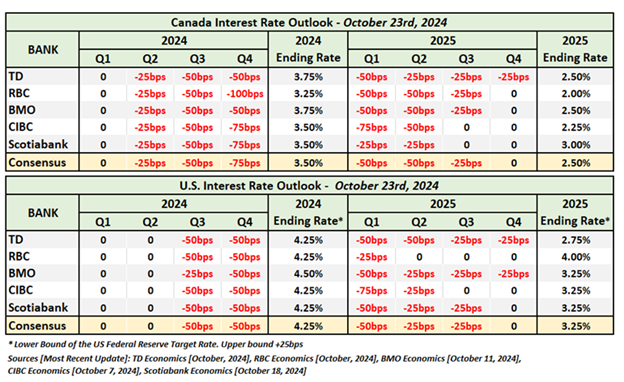

Current projections suggest that by the end of Q2 2025, we could see a reduction of approximately 100 basis points (1%) in interest rates in both Canada and the US.

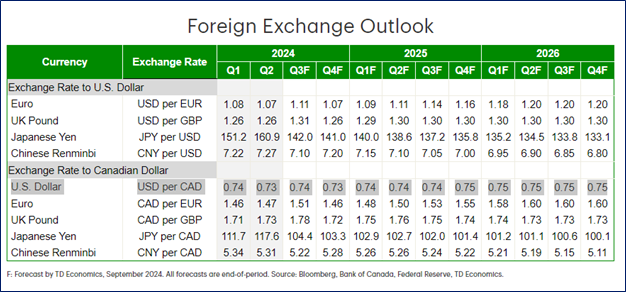

With both the Federal Reserve and Bank of Canada expected to cut rates in tandem, the US/CAD exchange rate is expected to remain stable.

5. Real Estate Market Dynamics

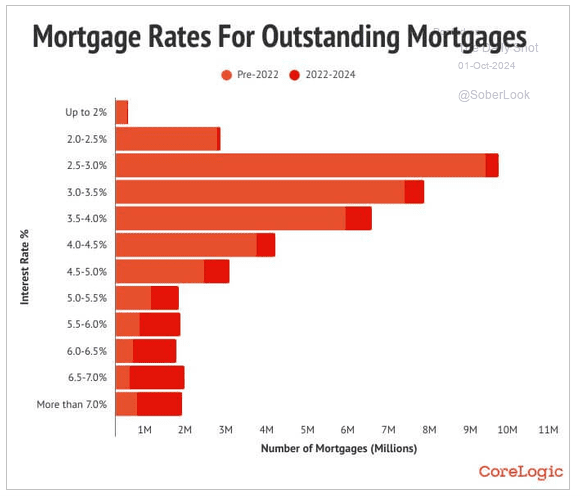

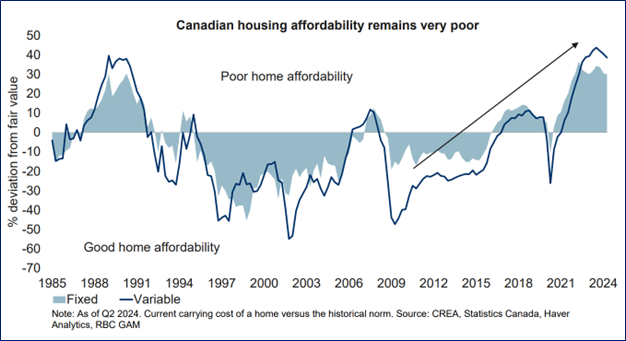

Real estate values have historically been affected by cash flows, which are driven by income and expenses. Higher interest rates and higher income and property taxes decrease real estate affordability.

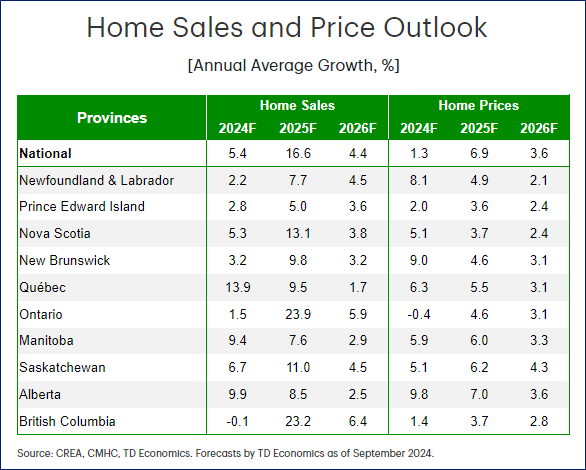

Forecasts indicate that market values and sales in British Columbia will remain flat through 2024 given these headwinds. However, as interest rate cuts begin to take effect, they may take pressure off of over-mortgaged homeowners with very few options out, and stimulate the flexibility we need to see a rebound in sales activity and gradual growth in home prices heading into 2025.

Despite these positive developments, housing affordability remains a significant concern. Canadian debt loads remain the highest in the world, suggesting that while conditions may improve, there’s still a long road to normalization.

Conclusion

In summary, as we approach the end of 2024, investors should keep a close eye on the evolving political landscape, economic indicators, and monetary policy shifts. While challenges remain, particularly in real estate affordability, the broader outlook suggests a more favourable environment for growth and investment as we transition into the new year.

You might also be interested in...

Estate Planning Misconceptions

In this 5-minute webinar, we explore an important but often misunderstood area of financial planning.

Learn More

Popular Categories

Search Insights

Book a meeting

Schedule a meeting with an RGF Advisor.